The Process of Annual Budget Preparation

The Process of Annual Budget Preparation

Annual budget for an organization is prepared for a year and is a comprehensive plan, a coordinated set of detailed financial statement of operating plans and schedule. It is the organization’s formal plan of action for the budgeted period. Annual budget is the best document for understanding the micro economics of the organization for the forthcoming budgeted period. Departmental budgets are the basis for the organization’s annual budget since it incorporates all the department’s budgets. It finally takes the shape of projected profit and loss statement and the balance sheet at the end of the budget period. It incorporates all the operating and the financial decisions.

In the budgeting process, the annual budget provides a single map explaining how the organization intends to earn profits and positive cash flow for the coming period. It also helps different departments of the organization to coordinate their activities so that together they can meet the overall goals and objectives of the organization in the budgeted period.

In an organization preparation of an annual budget is a daunting yet extremely important task. By definition, preparing the budget entails hard choices. These can be made, at a cost, or avoided, at a far greater cost. It is important that the necessary trade-offs be made explicitly when formulating the budget. This will permit a smooth implementation of priority programs, and avoid disrupting program management during budget execution. The annual budget is a comprehensive planning document that incorporates several other individual budgets. The annual budget is usually classified into two individual budgets namely the operational budget and the financial budget.

The annual budget formulation process has the following four major dimensions.

- To set up of the fiscal targets and level of expenditures compatible with targets. This is the objective of preparing the macro economic framework.

- Formulation of the expenditure policies.

- Allocating resources in conformity with both policies and fiscal targets. This is the main objective of the core processes of budget preparation.

- Addressing operational efficiency and performance issues.

Annual budget is the formal operating plan expressed in financial terms. Annual budget helps the management with respect to the following issues.

- Planning for the future and setting of the goals

- Motivating the employees of the organization

- Coordinating the activities between the departments of the organization

- Identification of the problem areas with performance evaluation

- Taking corrective actions in the areas where difficulties are expected

Annual budget is usually made for coming financial year. However actual performance against the budget is reviewed on a regular basis. In case there is any change in budget assumptions due to change in internal and external conditions, then some organizations undergo midterm revision in the annual budget.

The annual budget usually consists of the following three parts.

- The operating budget

- The capital expenditure budget. This includes expenditure on AMR (addition, modification and replacement) schemes

- The cash or financial budget.

Annual budget helps an organization to plan and coordinate all of the different budgets needed to run the organization. It includes budgets for sales, marketing, production, purchase, overhead expenses, an income statement, a cash flows statement and a balance sheet.

The budgeting process is an all encompassing task that brings in focus all short and long run goals and objectives of the organization. The process of preparing a budget compels management to explicitly recognize and assign quantitative values to all marketing, production, and financial decisions. A major reason for preparing annual budget is to obtain a measure of the impact of interrelated decisions on net income, financial position, and cash flow. However, the benefits of budgeting extend beyond the expression of decisions into numbers. Benefits of the annual budgeting process include the following.

- Recognition/improvement of organizational structure

- Increased emphasis on setting of long term objectives

- Increased motivation of the employees to achieve objectives

- Explicit recognition of important decision relationships

- Better coordination of activities between departments

- Improved organizational performance

- Better performance evaluation

The success of the budgeting process depends on the cooperation of all departments and all employees. The preparation of budgets follows a sequence in which departmental estimates based on sales forecasts are received and combined into an annual budget for the organization. This annual budget is approved by the top management.

Steps in the making of annual budget

The first step in making of the annual budget is to forecast the sales and fix the sale targets. The sales target and the production targets are to be co ordinate with each other. Both the targets are to be made product wise. Sales target is to take into consideration the sales realization. Sales realization for different product is to be based on historical trend and market projections.

After freezing the sale forecast, marketing budget is to be made for the year. It is to include the advertizing and sales promotion budget and the incentives to be given to the customers. It should also take into account any credit sales which are planned for the year. Sales budget will include any expenditure made for marketing of the product and department wage bill for the budget year.

Based on the sales target Production plans are made. Production plan takes into consideration starting inventory of the product at the beginning of the year and the desired inventory at the end of the budget year. Along with the production plan, norms for various production parameters such as yields, handling losses, and specific consumption of raw materials, fuel, energy, power, utilities, refractories, water, and consumables etc. Along with production plan, maintenance plan is also to be made. From these two plans requirements of raw materials, fuel, energy, power, utilities gases, refractories, water, consumables, operating parts and spare parts are to be worked out. During the calculation of the requirements, the safe inventory level of the materials at the stores is to be considered. These requirements are forwarded to the respective departments for the preparation of their budgets.

The last part of the annual budget is the budgeted income statement. It is based on the sales forecast and the cost data contained in the operating budgets. Budget cost sheets are prepared to measure the efficiency of the operating departments. Budgeted income statement estimates the expected operating income from the budgeted operations. It also provides management a vision of the likely operating results upon completing the budgeted operations. Financial ratios are used to assess the contribution of various budgeted items of the income statement to profitability, and to analyze the anticipated liquidity, leverage and return on equity portrayed by the budgeted balance sheet.

The next part of the organizational annual budget includes the financial budget. The financial budget consists of the following two individual budgets.

- Cash budget – Cash budget shows the effects of all the budgeted activities on cash. By preparing a cash budget, the organization is able to ensure that it has sufficient cash on hand to carry out activities. It also allows the management enough time to plan for any additional financing which might be needed during the budget period, and to plan for investments if there is excess cash. A cash budget includes all items that affect the cash flow and should also include three major sections namely cash available, cash disbursements, and financing.

- Budgeted balance sheet – This is the last step in the preparation of the annual budget. This is the sheet that shows the expected financial position at the end of the budget period.

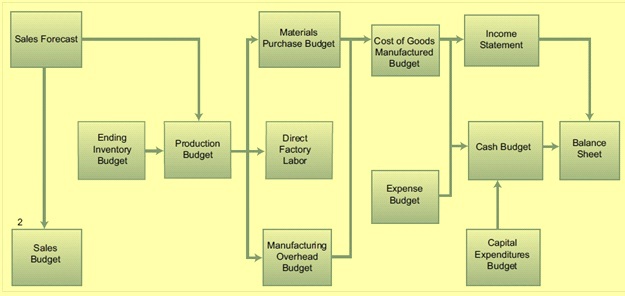

Typical process of preparing the annual budgets showing its important components is at Fig. 1

Fig 1 Typical process for preparation of annual budget

Budget performance reports compare budgeted figures with actual results. They reveal problem areas and help management correct them, as well as improve estimation methods. Because of the role of external factors, management is not always blamed for shortfalls. Nevertheless, it is essential that budgets contain achievable targets which motivate employees avoiding frustration which unmet goals can cause.

Leave a Comment